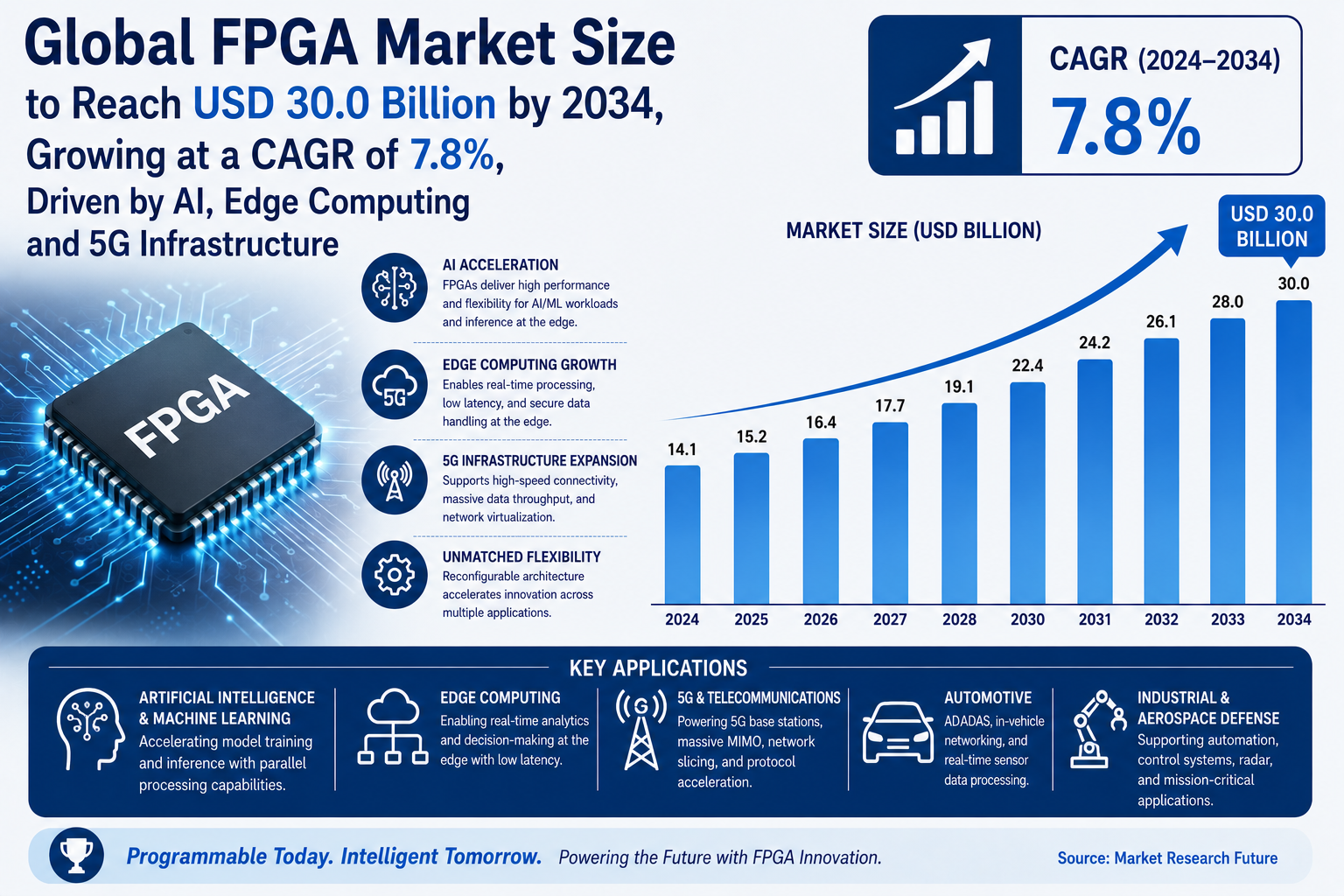

Global FPGA Market Size to Reach USD 30.0 Billion by 2034, Growing at a CAGR of 7.8%, Driven by AI, Edge Computing and 5G Infrastructure

According to a new report from Intel Market Research, the global FPGA market was valued at USD 15.2 billion in 2025 and is projected to reach USD 30.0 billion by 2034, growing at a robust CAGR of 7.8 % during the forecast period (2025‑2034). This momentum is driven by accelerating adoption of artificial‑intelligence inference, edge‑computing workloads, and 5G infrastructure, coupled with heavy investments from leading silicon vendors in advanced process nodes and heterogeneous integration technologies.

Field‑Programmable Gate Arrays (FPGAs) are reconfigurable silicon devices that enable hardware acceleration, low‑latency processing, and rapid prototyping across data‑center, automotive, aerospace, and industrial‑IoT applications. Their unique ability to be programmed post‑silicon empowers system architects to update algorithms, add features, and respond to evolving standards without redesigning the hardware, a characteristic that has become increasingly valuable in today’s fast‑moving technology landscape.

📥 Download FREE Sample Report:

FPGA Market - View in Detailed Research Report

What is FPGA?

Field‑Programmable Gate Arrays are integrated circuits that consist of an array of programmable logic blocks, configurable interconnects, and embedded hard IP (such as high‑speed transceivers, memory controllers, and DSP engines). Unlike fixed‑function ASICs, an FPGA can be programmed and re‑programmed throughout its lifecycle, allowing designers to tailor the hardware to specific workloads, implement custom accelerators, and perform iterative development cycles with dramatically reduced time‑to‑market. This flexibility is especially critical for emerging domains-AI‑driven edge inference, 5G base‑station signal processing, and autonomous‑vehicle sensor fusion-where algorithmic changes are frequent and hardware must keep pace.

The report provides a comprehensive view of the global FPGA market, covering macro‑level market size, competitive dynamics, technology trends, segmentation, regional performance, and strategic recommendations for stakeholders seeking to capitalize on the market’s growth potential.

Key Market Drivers

1. Surge in Edge‑AI and 5G Deployments

The explosion of edge‑AI workloads, ranging from smart cameras to industrial IoT gateways, requires low‑latency, high‑throughput compute that can be updated in the field. FPGA’s reconfigurable fabric delivers precisely that, enabling AI inference engines to be tuned for new models without hardware replacement. Simultaneously, telecom operators rolling out 5G infrastructure rely on FPGAs to accelerate digital front‑end processing, massive MIMO beamforming, and network‑slicing functions, creating a compound annual growth effect that exceeds 12 % in the next five years.

2. Data‑Center Acceleration Demand

Hyperscale cloud providers are increasingly offering FPGA‑based instances to meet the rising demand for workloads such as video transcoding, genomics analysis, high‑frequency trading, and AI inference. FPGAs can deliver up to 20× performance gains over traditional CPUs while maintaining superior power efficiency, making them a cost‑effective alternative for compute‑intensive services. Major cloud vendors now include FPGA instances in their service portfolios, reinforcing the technology’s position as a cornerstone of modern data‑center architectures.

3. Advancements in Design Toolchains

The maturation of high‑level synthesis (HLS) frameworks and expanded ecosystem support-from vendor‑provided IP libraries to open‑source toolchains-has lowered the barrier for software‑engineers to target FPGA hardware. This democratization of design expertise shortens development cycles, broadens the talent pool, and accelerates time‑to‑market for new products across multiple verticals.

➤ “Flexibility without sacrificing performance has become the cornerstone of modern compute architectures.”

Market Challenges

Complexity of Design Flows

Despite the availability of HLS tools, many organizations still view FPGA development as a niche skill requiring deep hardware knowledge. This perception can translate into longer project timelines and higher engineering costs, particularly for small‑to‑mid‑size enterprises that lack dedicated FPGA experts.

Cost Sensitivity in Consumer Electronics

Consumer‑electronics manufacturers prioritize ultra‑low unit cost and high volumes. In such markets, fixed‑function ASICs often outperform FPGAs on a cost‑per‑die basis, limiting FPGA penetration for applications where price per unit must remain below a few dollars.

Supply‑Chain Constraints

Global semiconductor shortages have intermittently restricted the availability of high‑performance FPGA families, extending lead times for premium devices to six months or more. Geopolitical tensions affecting key fab locations further introduce uncertainty in capacity planning, prompting OEMs to maintain higher inventory buffers and potentially eroding profitability.

Emerging Opportunities

Automotive ADAS and Autonomous Driving

Advanced driver‑assistance systems (ADAS) and autonomous‑driving platforms demand deterministic latency, high‑speed sensor fusion, and over‑the‑air (OTA) update capability. FPGAs satisfy these requirements by offering a single hardware platform that can host multiple functions-radar processing, camera pipelines, and vehicle‑to‑infrastructure communication-while remaining certifiable under functional‑safety standards such as ISO 26262.

Aerospace, Defense, and Rugged Applications

Mission‑critical aerospace and defense programs seek radiation‑tolerant, secure, and long‑life silicon. FPGA families that incorporate hardened transceivers, encrypted bit‑streams, and tamper‑resistance are gaining traction for radar, electronic‑warfare, and secure‑communication systems, creating a niche yet high‑value market segment.

Next‑Generation Process Nodes

Investments in 7 nm, 5 nm, and emerging EUV‑based FPGA families promise lower power envelopes, higher logic densities, and new hard AI blocks. These advances unlock application classes such as blockchain acceleration, real‑time analytics at the edge, and ultra‑low‑latency financial trading.

Segment Analysis

| Segment Category | Sub‑Segments | Key Insights |

| By Type |

|

Low‑Power FPGAs

|

| By Application |

|

Data‑Center Acceleration

|

| By End User |

|

OEMs

|

| By Architecture |

|

Hybrid Architecture

|

| By Industry |

|

Aerospace & Defense

|

Competitive Landscape

Global FPGA Market Competitive Overview 2024

The FPGA market remains dominated by two legacy titans-AMD (through its Xilinx portfolio) and Intel (via the Altera acquisition). AMD’s Xilinx line leads in high‑performance, data‑center, and AI‑centric devices, leveraging an adaptive compute architecture and a robust ecosystem of design tools. Intel’s strategy focuses on tightly integrating FPGA fabric with its Xeon CPUs and programmable acceleration platforms, targeting cloud infrastructure, networking, and edge‑computing workloads. Both companies benefit from deep R&D investments, extensive IP libraries, and global sales networks that reinforce their market leadership and create high entry barriers for newcomers.

Beyond the duopoly, a vibrant tier of niche innovators adds depth to the competitive landscape. Lattice Semiconductor excels in low‑power, cost‑sensitive segments such as IoT and mobile applications, while Microchip Technology (through Microsemi) serves aerospace and defense markets with ruggedized solutions. Achronix provides high‑bandwidth, high‑performance FPGAs for data‑intensive workloads, and QuickLogic focuses on ultra‑low‑power sensor processing. Additional players-including Broadcom, NXP, Samsung, Marvell, Cypress Semiconductor, and Renesas-offer specialized programmable logic blocks integrated with their broader semiconductor portfolios, addressing automotive, communications, and industrial use cases.

List of Key FPGA Companies Profiled

-

Achronix

-

QuickLogic

-

Broadcom

-

NXP Semiconductors

-

Samsung Electronics

-

Marvell Technology Group

-

Cypress Semiconductor

-

Renesas Electronics

Market Trends

Rise of AI‑Driven Edge Computing

Increasing demand for real‑time inference at the network edge is reshaping the FPGA market. Designers are turning to reconfigurable hardware because it delivers low‑latency processing while maintaining power efficiency- a combination that traditional ASICs struggle to match. Recent product launches from leading vendors emphasize hardened AI blocks, enabling developers to embed neural‑network accelerators directly within the FPGA fabric. This integration shortens time‑to‑market for edge devices such as smart cameras and industrial gateways and supports OTA updates that keep algorithms current without hardware replacement.

Increased Use in Automotive Systems

Automotive manufacturers embed FPGAs to meet stringent safety standards and support advanced driver‑assistance systems (ADAS). The programmable nature of the devices allows a single hardware platform to host multiple functions-sensor fusion, radar signal processing, high‑definition video compression-while adhering to functional‑safety guidelines (ISO 26262). As vehicle electrification progresses, the need for flexible computing resources grows, prompting a shift from fixed‑function silicon to adaptable solutions that evolve with software updates throughout a vehicle’s lifecycle.

Expansion into 5G Infrastructure

Telecommunications operators leverage the FPGA market to accelerate the rollout of 5G core and transport networks. The ability to reprogram logic on demand enables rapid adaptation to evolving protocol standards and spectrum allocations. In base‑station hardware, FPGAs provide high‑throughput digital front‑end processing, supporting massive MIMO configurations and beamforming algorithms. Their deterministic performance also makes them attractive for network slicing, where isolated virtual networks require dependable low‑latency processing for diverse service classes.

Regional Analysis

North America

North America remains the most prominent region in the FPGA market, driven by substantial R&D investments, a strong presence of defense and aerospace programs, and a highly skilled technology workforce. The region’s mature ecosystem supports innovation in data‑center acceleration, edge AI, and 5G infrastructure, reinforced by the headquarters and regional sales networks of leading vendors.

Europe

Europe exhibits solid growth, propelled by automotive, aerospace, and industrial automation demand. European initiatives focusing on energy efficiency and sustainable technologies create new FPGA opportunities in smart‑grid applications and renewable‑energy control systems. Government‑backed digitalization programs further stimulate market expansion.

Asia‑Pacific

Asia‑Pacific is the fastest‑growing region, fueled by rapid industrialization, massive 5G rollout, and a burgeoning consumer‑electronics market. China, Japan, South Korea, and Taiwan are emerging as major design and manufacturing hubs for FPGA silicon. While geopolitical tensions pose risks, the region’s focus on AI, IoT, and high‑performance computing sustains robust demand.

South America

South America presents a modest but growing FPGA market, underpinned by investments in telecommunications infrastructure, mining automation, and expanding data‑center footprints. Regional government initiatives aimed at technology adoption are expected to stimulate further demand.

Middle East & Africa

The Middle East & Africa region is nascent yet promising, driven by infrastructure projects in telecommunications, defense, and smart‑city development. Strategic diversification efforts and increasing digital adoption create fertile ground for FPGA‑based solutions.

Report Deliverables

- Comprehensive global and regional market size (historical & forecast) for 2025‑2034.

- In‑depth segmentation by type, application, end‑user, architecture, and industry.

- Qualitative and quantitative analysis of market drivers, challenges, and opportunities.

- Competitive landscape with company profiles, market‑share estimates, and strategic initiatives (M&A, partnerships, product launches).

- Technology roadmap highlighting upcoming process nodes, hard AI blocks, and heterogeneous integration trends.

- Strategic recommendations for investors, OEMs, and system integrators seeking to capitalize on growth corridors.

📘 Get Full Report Here:

FPGA Market - View Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

- Real-time competitive benchmarking

- Global clinical trial pipeline monitoring

- Country-specific regulatory and pricing analysis

- Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us

Κατηγορίες

Διαβάζω περισσότερα

Best Hotels in Doha offer an exceptional blend of luxury, comfort, modern amenities, and world-class hospitality. Whether you're traveling for business, a family vacation, a romantic getaway, or a cultural adventure, Doha features a wide range of accommodations to suit every budget and travel style. From elegant five-star resorts to boutique hotels and family-friendly properties,...

Industrial automation systems require efficient and reliable directional control components, and a Single Acting Pneumatic Valve is widely used for controlled airflow regulation with spring-return functionality, while this Single Acting Pneumatic Valve provides stable operation, simplified structure, and efficient performance in packaging machinery, light industrial automation, and fluid...

THE CHARM OF AJMER ESCORT SERVICES Ajmer, A City Known For Its Spiritual Significance And Historical Beauty, Also Harbors A Secret World Of Pleasure And Desire. The Ajmer Call Girl Service Offers Sophisticated Escort Services For Those Who Crave Sexual Fulfillment And Intimate Connections Beyond The Ordinary. Our Hot Milf Women Provide Unforgettable Experiences Tailored To Your...

Adwysd Joggers Are Changing the Future of Casual Fashion Streetwear is no longer limited to skate parks or city streets. It has become a global fashion movement that combines comfort, confidence, and individuality. Among the brands making an impact in this space, Adwysd has built a reputation for creating clothing that feels as good as it looks. Adwysd Joggers represent this vision perfectly by...

According to a new report from Intel Market Research, the global AI Satellite Data Analytics market was valued at USD 3.85 billion in 2025 and is projected to grow from USD 4.31 billion in 2026 to USD 9.76 billion by 2034, exhibiting a robust CAGR of 11.8% during the forecast period (2025‑2034). This growth is propelled by the rapid expansion of satellite constellations, exponential...