The bus chassis market in right-hand drive (RHD) countries is undergoing rapid expansion as governments and transportation authorities prioritize sustainable mobility, urban transit modernization, and low-emission transportation systems. Increasing population density, rising urban congestion, infrastructure development, and technological innovation are significantly influencing demand for advanced bus chassis platforms across major RHD economies.

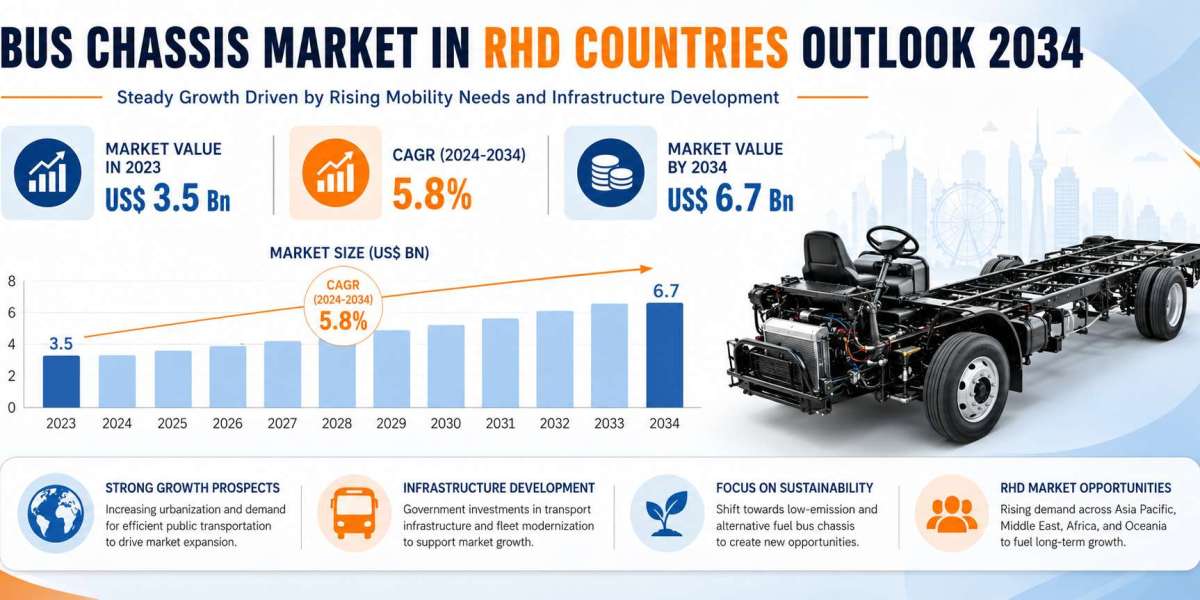

The market was valued at approximately US$ 3.5 billion in 2023 and is expected to reach nearly US$ 6.7 billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.8% during the forecast period. This growth reflects increasing investments in public transportation infrastructure, expanding electric bus adoption, and the modernization of existing transit fleets in countries such as India, Japan, Australia, the United Kingdom, South Africa, Malaysia, Thailand, Singapore, and New Zealand.

A bus chassis forms the structural and mechanical foundation of a bus. It supports the body structure, engine, drivetrain, suspension, steering, and braking systems while ensuring operational durability and passenger safety. The chassis is one of the most critical components in determining the performance, fuel efficiency, ride quality, and longevity of commercial buses.

As transportation systems evolve, manufacturers are redesigning bus chassis platforms to accommodate new propulsion technologies, advanced safety systems, digital connectivity, and lightweight materials. These innovations are helping transit operators improve operational efficiency while meeting increasingly stringent environmental regulations.

Urbanization remains one of the strongest drivers of the bus chassis market in RHD countries. Cities across Asia Pacific, the United Kingdom, and Africa are experiencing rapid population growth, creating immense pressure on existing transportation infrastructure. Public transportation networks are therefore expanding to improve mobility, reduce traffic congestion, and minimize environmental impact.

Buses continue to serve as one of the most cost-effective and scalable transportation solutions for densely populated urban areas. Governments are heavily investing in city bus services, bus rapid transit (BRT) systems, and intercity transportation corridors to support economic growth and urban development. This surge in public transportation projects is directly increasing demand for durable and efficient bus chassis platforms.

India has emerged as the largest market within the Asia-Pacific region due to its growing urban population and large-scale public transportation initiatives. Metropolitan regions such as Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad are expanding bus fleets to address rising commuter demand. Government programs promoting electric mobility and clean public transportation are further accelerating bus procurement activities.

The country’s strong automotive manufacturing ecosystem also supports market growth. India hosts several leading commercial vehicle manufacturers and component suppliers, enabling large-scale production of bus chassis for domestic and export markets. Competitive manufacturing costs, skilled labor availability, and government incentives continue to strengthen India’s position as a global bus manufacturing hub.

Environmental sustainability has become a key priority for governments worldwide, and this is significantly shaping the bus chassis industry. Strict emission regulations are encouraging transit operators to replace older diesel buses with cleaner alternatives powered by hybrid, electric, or alternative fuel technologies.

In countries such as the United Kingdom and Japan, regulatory bodies are implementing aggressive targets to reduce greenhouse gas emissions from public transportation systems. Clean air initiatives and low-emission zones in major cities are pushing fleet operators toward low-carbon mobility solutions. As a result, manufacturers are developing bus chassis platforms optimized for electric and hydrogen-powered buses.

Electrification is rapidly becoming one of the defining trends in the bus chassis market. Electric buses are gaining popularity because they offer lower operating costs, reduced emissions, and quieter operation compared to traditional diesel-powered vehicles. Governments are also introducing subsidies and incentive programs to accelerate electric bus deployment.

Electric bus chassis require specialized engineering to integrate battery systems, electric motors, thermal management systems, and charging infrastructure. Unlike conventional diesel chassis, electric platforms must distribute battery weight efficiently while maintaining structural stability and passenger safety. This has encouraged manufacturers to invest heavily in modular and lightweight chassis architectures.

Several global manufacturers are actively introducing next-generation electric bus platforms. Scania launched a battery-electric bus chassis platform capable of supporting energy storage capacity of up to 520 kWh with an operational range of approximately 500 kilometers. Mercedes-Benz also introduced the eO500U electric chassis platform for urban transit applications. These innovations highlight the industry’s transition toward sustainable mobility solutions.

Technological advancements are playing a critical role in modern bus chassis development. Manufacturers are increasingly integrating advanced driver assistance systems (ADAS), telematics, remote diagnostics, and intelligent fleet management solutions into commercial bus platforms. These technologies improve vehicle safety, operational efficiency, and maintenance planning.

Advanced safety features such as collision warning systems, electronic stability control, adaptive cruise control, lane departure warnings, and automated emergency braking are becoming standard in modern buses. Transit agencies are prioritizing passenger safety and operational reliability, especially in densely populated urban environments.

Connected vehicle technologies are also transforming fleet management practices. Real-time monitoring systems allow operators to track vehicle performance, fuel consumption, battery condition, maintenance schedules, and driver behavior. Predictive maintenance capabilities help minimize downtime and reduce operational costs by identifying potential technical issues before they lead to major failures.

Passenger comfort is another important factor influencing chassis design. Modern commuters expect comfortable seating, air conditioning, low-noise cabins, smooth ride quality, onboard Wi-Fi, and entertainment systems. To meet these expectations, manufacturers are investing in improved suspension systems, vibration reduction technologies, and advanced structural engineering.

Among various chassis frame types, ladder frame chassis continue to dominate the market due to their strength, affordability, and adaptability. Ladder frame designs are particularly suitable for emerging economies where road infrastructure quality can vary significantly. Their rugged construction enables buses to operate effectively under harsh road conditions and heavy passenger loads.

The flexibility of ladder frame chassis also allows manufacturers to customize bus configurations according to specific operational requirements. This makes them highly popular across school buses, city buses, rural transport vehicles, and intercity coaches.

At the same time, modular frame platforms are gaining traction in premium and electric bus categories. Modular chassis architectures enable manufacturers to standardize production processes while supporting multiple propulsion technologies and body configurations. These platforms improve manufacturing efficiency and reduce overall development costs.

Material innovation is becoming increasingly important as manufacturers seek to improve fuel efficiency and electric vehicle range. Steel remains the dominant chassis material because of its durability and cost-effectiveness. However, high-strength steel and aluminum alloys are gaining popularity due to their lightweight properties and enhanced structural performance.

Reducing vehicle weight is especially critical for electric buses because lighter chassis platforms improve battery efficiency and operational range. Composite materials are also being explored for specialized structural applications where corrosion resistance and weight reduction are important considerations.

The bus chassis market serves multiple vehicle categories, including school buses, coaches, minibuses, articulated buses, double-decker buses, low-floor buses, and shuttle buses. Each segment requires specific chassis engineering solutions depending on passenger capacity, route conditions, and operational objectives.

Low-floor buses are increasingly favored in urban transportation systems because they improve accessibility for elderly passengers and people with disabilities. These buses require specially designed chassis platforms that support low entry heights while maintaining vehicle stability and passenger comfort.

Coach and luxury bus segments are also experiencing growth, particularly in countries with strong tourism industries and long-distance transportation demand. Premium coaches require chassis platforms capable of delivering smooth ride quality, enhanced luggage capacity, high-speed stability, and superior passenger comfort.

Asia Pacific remains the dominant regional market for bus chassis in RHD countries. India, Japan, Australia, and New Zealand collectively account for a significant share of global demand due to expanding public transportation infrastructure and rising investments in electric mobility solutions.

ASEAN countries such as Malaysia, Thailand, and Singapore are also witnessing strong market growth driven by urbanization, industrialization, and tourism-related transportation demand. Governments across the region are investing in smart city initiatives and modern transit systems to improve urban mobility.

The United Kingdom continues to emerge as an important market for electric buses and low-emission transportation systems. Government-backed zero-emission bus programs and clean air regulations are accelerating fleet electrification efforts among transit operators.

Africa and Latin America are expected to present long-term opportunities for market participants as urban populations expand and governments invest in transportation infrastructure modernization. Although diesel-powered buses currently dominate these regions, gradual adoption of cleaner propulsion technologies is anticipated over the coming decade.

Competition within the bus chassis market is intensifying as manufacturers focus on innovation, strategic partnerships, and geographic expansion. Major industry participants include Tata Motors, Ashok Leyland, Volvo, Daimler AG, Hyundai Motor Company, Scania, IVECO, MAN, Dongfeng Motor Company, and BharatBenz.

Manufacturers are increasingly collaborating with transit authorities, charging infrastructure providers, and technology companies to strengthen their market position. Partnerships involving electric mobility ecosystems, digital fleet management platforms, and sustainable transportation projects are becoming increasingly common.

Recent developments reflect the industry’s ongoing transformation. Tata Motors secured a major order from the Uttar Pradesh State Road Transport Corporation to supply 1,350 BS6-compliant diesel bus chassis for intercity transportation services. Volvo Buses India introduced the next-generation Volvo 9600 platform designed for premium sleeper and seater coach applications. Such product launches demonstrate the growing focus on both sustainable mobility and passenger comfort.

Despite strong growth prospects, the market faces certain challenges. Electric bus deployment requires substantial investments in charging infrastructure, battery technology, and grid modernization. High upfront costs remain a concern for some transit operators, particularly in developing economies.

Supply chain disruptions, fluctuating raw material prices, and semiconductor shortages can also impact production schedules and profitability. Additionally, transitioning to electric mobility requires workforce retraining and the development of specialized maintenance capabilities.

Nevertheless, the long-term outlook for the bus chassis market in RHD countries remains highly positive. Continued urbanization, increasing government support for sustainable transportation, technological innovation, and rising environmental awareness are expected to sustain strong market growth throughout the forecast period.

Manufacturers that successfully deliver durable, lightweight, energy-efficient, and digitally connected chassis solutions will likely gain a competitive advantage as the global transportation industry continues evolving toward cleaner and smarter mobility systems.